How Your Brain Influences Your Financial Life

Let's Transform Your Relationship with Money

Do you remember when you were a child and got so engrossed in something that it was as if the world around you didn’t exist?

For me, that was drawing; for my brother, it was video games (I’ll have to ask my sister what her ‘thing’ was).

I remember standing a few feet away from him and calling his name, and it usually took the third or fourth time and yelling his name to get his attention.

That’s how I feel when reading/learning about the connection between money and the brain. Neuroscience has 100% been the missing piece of the puzzle for me - and the more I know, the more I want to share.

The connection between neuroscience and money isn't just an interesting theory—it's the key to transforming our relationship with money.

In case you missed it, I published this article, which should give you a basic start to understanding neuroscience and how we create neural pathways that shape our behaviors (as well as how we can change them).

I love discovering that so many of our money behaviors aren't just habits—they're neurologically hardwired patterns that began forming when we were children.

The connection between neuroscience and money isn't just an interesting theory—it's the key to transforming our relationship with money.

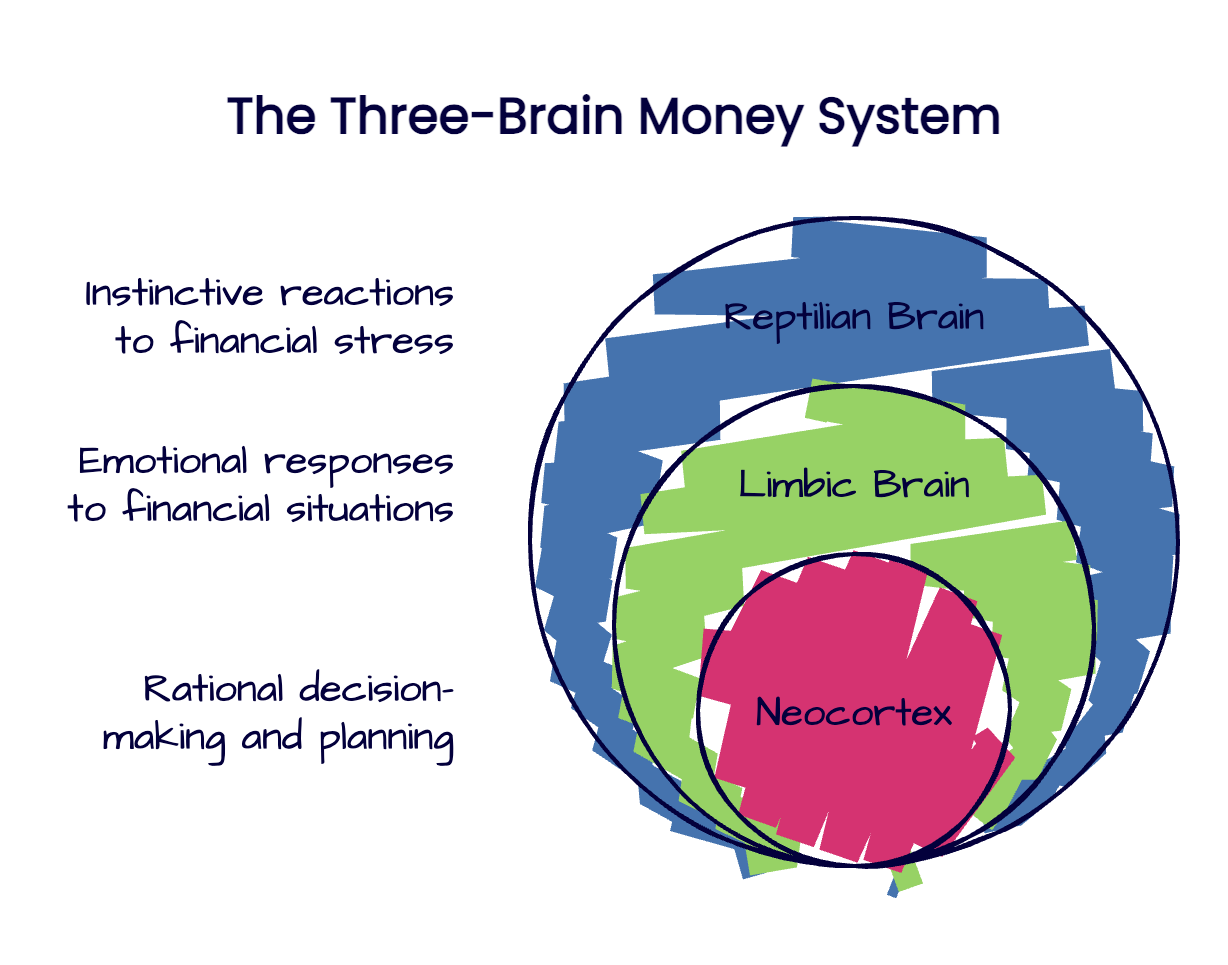

The Three-Brain Money System

Did you know that you actually have three distinct "brains" that influence your financial decisions? Let me break it down for you:

1. Your Reptilian Brain (Survival Mode)

This is your oldest, most primitive brain structure. It's constantly on high alert for threats and operates from instinct rather than logic. When financial stress triggers this part of your brain, you go into fight, flight or freeze mode.

Ever notice how a past-due bill can send you into a panic or freeze you into inaction? That's your reptilian brain taking over.

2. Your Limbic Brain (Emotional Mode)

This is your feeling brain—where emotions around money live. Those feelings of shame when you can't afford something, the joy of an unexpected windfall, or the anxiety about retirement all come from here.

The limbic system is why we make emotionally driven purchases we later regret. Remember those shoes you absolutely "had to have" but never wear? Thank your limbic brain for that decision.

3. Your Neocortex (Thinking Mode)

This is your rational brain—the one that can plan, analyze, and make thoughtful financial decisions. It's the part we want in charge of our money choices, but it's often overridden by the other two.

When we look at a retirement calculator and logically plan our savings strategy—that's the neocortex at work.

Why Financial Education Isn't Enough

This explains why simply learning about compound interest or budgeting apps often doesn't translate into lasting change (especially if you have an aversion to spreadsheets… me. I’m talking about me 😉). The information might reach your thinking brain, but your decisions are still driven by those deeper, more primitive brain structures that formed their money patterns decades ago.

Financial literacy alone doesn't address money's emotional charge or the survival-level responses it triggers. That's why I'm so passionate about approaching money from both angles—practical knowledge and psychological understanding.

How Your Brain Gets Wired Around Money

Most money patterns were unconsciously formed between ages 2-12 when our brains developed rapidly. During this time, we absorbed not just the explicit messages our families told us about money but the implicit ones, too:

The tension in your mother's voice when bills arrived

The arguments between your parents about spending

The celebration or stress around payday

The silence when you asked questions about family finances (if you even asked, or where you scared?)

These experiences create neural pathways—actual physical connections in your brain—that determine how you respond to money situations as an adult. The more these pathways fire, the stronger and more automatic they become.

The Chemistry of Money Stress

Financial stress triggers a flood of cortisol (the stress hormone) in your brain.

Too much cortisol is toxic to your brain cells. It impairs decision-making (the only thing I’ve ever read/heard about cortisol is that it causes people to gain or retain weight…probably so the weight loss industry can sell you something that doesn’t work).

This creates a vicious cycle: money stress leads to poor decisions, which creates more money stress.

Meanwhile, shopping or purchasing can trigger dopamine release—the "feel good" neurotransmitter. This explains why retail therapy provides temporary relief from financial anxiety, even when it worsens your situation long-term.

The good news?

Neuroplasticity.

Neuroplasticity is the most empowering concept I've discovered in my money journey.

Think of neuroplasticity as your brain's lifelong ability to create new pathways—like carving fresh trails through a forest. Even those money patterns formed at the kitchen table while listening to your parents argue about bills can be reshaped and redirected.

I find it almost poetic that the same brain that absorbed those early money messages has the built-in capacity to transform them. 🤯

Remember when we all believed that "you can't teach an old dog new tricks"? Well, science has completely flipped that notion upside down. Your incredible brain continues creating new connections whether you're 35, 54 (like me!), or 78.

Each time you pause before an impulse purchase or practice self-compassion around a financial misstep, you're literally building alternative routes in your neural network. It's like your brain says, "I see this new path you're creating, and I'm going to make it stronger each time you use it."

Those money patterns that feel so profoundly "hardwired" are more like Play-Doh than concrete—ready to be reshaped with gentle, consistent practice.

What's Your Money Brain Pattern?

Take a moment to consider which part of your brain tends to dominate your financial life:

Do you make impulsive money decisions based on fear or security? (Reptilian)

Are your financial choices driven primarily by emotions like guilt, shame, or comfort? (Limbic)

Do you approach money with logical analysis but struggle to follow through on your plans? (Neocortex with limbic override)

In next week's newsletter, I'll share some specific techniques to help rewire your money brain for better financial outcomes. We'll explore practical exercises that work with your brain's natural patterns rather than against them.

A Woman You Should Know

Dr. Tara Swart

She is a neuroscientist, medical doctor, and executive coach who studies the intersection of neuroscience and financial behavior. Her book “The Source” explores how we can harness neuroplasticity to create lasting change in our lives, including our financial patterns. As a woman in a male-dominated field, she's breaking barriers while making neuroscience accessible to everyone.

Money Moves

Now that we understand our three-brain system, here's a simple practice to try this week: The 10-Second Pause.

When you're about to make a financial decision, take 10 seconds to breathe deeply. This gives your thinking brain (neocortex) time to catch up with your emotional and survival brains, which react much faster. During this pause, ask yourself: "Which part of my brain is making this decision right now?"

Creating this awareness can help shift financial decisions from your reptilian or limbic brain to your more rational neocortex.

Resources

Newsletter 📃

I love sending and receiving handwritten notes. “This newsletter will inspire and encourage the art of writing heartfelt notes and letters and help you uncover your own "voice." Read and subscribe to “The Heartspoken Note” by

.Book 📕

Jason Zweig's Your Money and Your Brain explores the surprising ways our brains influence financial decisions, often causing smart people to make costly mistakes. Blending entertaining experiments and real-world stories, the book offers practical strategies to help investors overcome emotional impulses and make smarter financial choices.

Podcast 📹

I’ve listened to this interview with Dr. Joe Dispenza on This Magic Life with Andrea Koppel three times in the last four days (yes, it’s that good). Dr. Joe shares his story in more detail than I’ve heard it before (healing his spine without surgery after being hit by a truck and told he’d probably never walk again) and creating the life you want. It's SO good. Listen/watch here.

#sorrynotsorry 🤣

Starting next week, all emails will come from Kit (I’ll still publish posts on Substack). I’m writing a post on the strategy for this in my other newsletter and will link to it when it’s done (if you’re interested).

Have a wonderful day,

Kim

Thank you so much for recommending my newsletter, Kim, and my work to promote the writing of handwritten notes. They matter!

I’ve already shared this excellent post. As a trained anatomist, I have done (decades ago) research in neuroplasticity, so I was fascinated with the information you provided about brain function. And having served on a regional bank board for over two decades, I know that financial education isn’t always enough. Understanding that our attitude about money is a complicated blend of physiology, environment, and upbringing — and the new belief that neurons can, indeed, be retrained—should give everyone hope that if their “relationship” with money isn’t what they want it to be, they can change!